What is productivity and why is it important?

It might be timely to rename the ‘productivity puzzle’ as the ‘productivity panic’, given the number of articles bemoaning the inability of the world’s major economies to escape from the synchronised stagnation of the last decade. As hopes of a post-Covid reset have receded, economists have become ever-more alarmed about slow growth. While there have been a few brighter spots in some recent data, nothing is coming near the growth rates of the late 20th century, upon which many of our economic assumptions were built.

But what exactly is it that these alarmed economists are worried about, and why?

How is productivity measured?

Productivity is a term often used interchangeably with ‘efficiency’. The mathematical definition of efficiency is a ratio of input to output. However, efficiency is often used in other contexts so has become something of an imprecise term.

Productivity is a measure of efficiency, of output per unit of input. Labour productivity is therefore a measure of the amount produced per worker or per hour worked.

The UK’s Office for National Statistics (ONS) defines labour productivity as:

It defines Gross Value Added (GVA) is the total value of output of goods and services produced less the intermediate consumption (goods and services used up in the production process in order to produce the output).

GDP differs from GVA as it is a measure of overall economic activity, so it is not as specifically focussed on production as GVA. However, the difficulty of getting timely GVA data internationally means that organisations like the OECD, IMF and World Bank usually use GDP per worker or per hour worked for country comparisons.

When looking at organisational level productivity, the ONS uses Gross Value Added divided by full-time equivalents (FTE). Organisations use a variety of measures for internal reporting, such as Value Add per FTE or Revenue per FTE.

Why is productivity important?

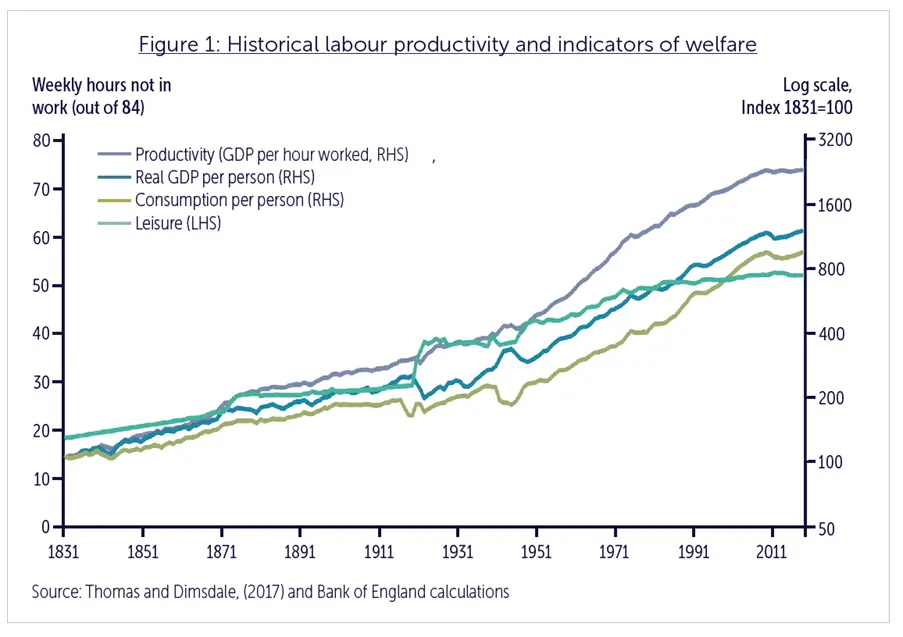

It has become something of a cliché to quote Paul Krugman when writing about why productivity is important but if you want to understand why productivity “is almost everything”, former Bank of England MPC member Silvana Tenreyro explains it in one chart.

Chart from “The fall in productivity growth: causes and implications”. Speech given by Silvana Tenreyro, External MPC Member, Bank of England

As she remarked:

Higher productivity is associated, almost mechanically, with higher GDP and consumption per person. Labour productivity is 25 times higher than in 1831. That has enabled a 12-fold increase in the level of GDP per person and a 9-fold increase in consumption per person. Those increases come despite spending less of our lives working. Leisure time, crudely measured as hours not in work, has increased from less than 20 hours a week in the 1830s to 50 hours a week today.

The history of human development is one of ever improving productivity. An improved standard of living and all the good things that go with it, such as health improvements, longer life expectancy, falling crime rates and more leisure time, have all come about because higher productivity has delivered more wealth per person. The more we have been able to produce for each hour worked, the safer, more comfortable and longer life has become.

That may be so at a whole economy level but why does productivity matter for individual organisations? It’s fair to say that, in many organisations, it doesn’t – or at least not in the short-term, which is why many don’t measure it. In certain circumstances it is possible to grow a business and increase profit even when your productivity per worker is falling, especially in markets where labour is plentiful, flexible and relatively cheap.

However, over the longer-term this could leave companies vulnerable to sudden changes in the market. New competitors or more expensive labour could threaten less productive companies. Increasing a firm’s productivity therefore acts as an insurance policy against short-term headwinds. Higher productivity firms are also those that are more likely to increase revenues and market share over time. One explanation for the UK’s recent rise in aggregate productivity is that recent sharp increases in costs have put the less productive firms out of business. As the Resolution Foundation’s Greg Thwaites explained:

“Since the financial crisis, and outside of the pandemic, creative destruction has been sluggish. Think of it this way. Interest rates were basically zero for over a decade. Energy was cheap. The minimum wage was low. If you were running a not-very-productive business, you could get by –maybe not thrive, but survive. Too many firms were limping along, tying up workers and capital that could have been used more productively elsewhere. That lack of churn is one of the prime suspects behind the UK’s productivity malaise.

“Now the environment has changed. Interest rates are higher, energy costs more, and the minimum wage has risen sharply. And sure enough, we’re seeing more firms go under. Job losses from exiting firms in 2024 were the highest since 2011. Corporate insolvencies are running well above pre-pandemic levels. Redundancies are up too.”

Economic circumstances enabled low productivity firms to stay in business for many years but, as Krugman said, in the long run, productivity is almost everything. Like so many things, ignoring productivity is fine until it isn’t.

Historically, leaps in productivity have come about through the deployment of new technologies, such as steam power and electricity. The advanced economies experinced unprecedented productivity growth after WW2, when wartime technologies were re-purposed for civilian use. A less dramatic boost happened with the rollout of IT in the 1980s and 90s. The hope now is that rapid advances in AI will provide the next productivity leap and break us out of the post-Financial Crisis stagnation.

Many are sceptical. This month, a study of 6,000 firms US, UK, Germany and Australia by the US National Bureau of Economic Research found that 80% of the firms reported little or no impact on productivity, over the last three years, from using AI. As the Chief Economist at Apollo asset mangement remarked, “AI is everywhere except in the incoming macroeconomic data. Maybe there is a J‑curve effect for AI, where it takes time for AI to show up in the macro data. Maybe not.”

The J-curve effect was a term first used by Professor Erik Brynjolfsson, a prolific writer on the relationship between technology and productivity, who described the effect of the investment needed in the organisational innovations required to exploit technology. This, he argued, causes a productivity dip before the productivity boost, which comes some time later.

“General purpose technologies (GPTs) such as AI enable and require significant complementary investments, including co-invention of new processes, products, business models and human capital.”

Studies of the last IT-enabled productivity boom in the 1990s found that the investment in organisation was as important, if not more so, than the investment in technology. Many firms threw money at technology. The ones that made productivity gains were those that also put significant resource into organisations, processes and people. As Nina Jorden, one of the speakers at our forthcoming event put it ‘productivity is a strategic capability’.

Where Reward comes in

Leading and incentivising organisational change is a major part of the Reward function’s role. If improving productivity is a strategic capability, Reward is key to developing, improving and retaining it.

The productivity paradox, the stubborn fact that massive technology investment hasn't translated into broad productivity growth, let alone improved organisational performance, suggests some fundamental changes are needed in organisations.

The problem isn't usually the technology. It's that organisations are layering new tools onto old structures, outdated role designs, and reward frameworks that were built for a different era. They're optimising parts of the system without rethinking the system itself. AI makes this even more acute. It can automate routine work at extraordinary speed, but if organisations don't redesign roles, redefine what good performance looks like, and realign how they measure and reward value: they'll simply become very efficient at the wrong things.

Most reward structures are still anchored to individual performance metrics and traditional job architectures. But the productivity challenge is systemic and organisational. Technology changes what work gets done, who does it, and how value is created. The entire logic of how we measure contribution and share value needs to evolve.

This is the gap that reward professionals are uniquely positioned to close. Not by tweaking incentive plans at the margins, but by asking the harder strategic questions:

- Are we measuring and rewarding the outcomes that actually drive organisational performance, or just the ones that are easiest to count?

- As technology reshapes roles and workflows, are our reward structures keeping pace, or reinforcing yesterday's ways of working?

- Are we treating AI as a tool that supports better human decision-making and organisational design, or as a substitute for the harder work of getting structures, incentives and culture right?

Getting the distinction clear: between productivity and performance*, between efficiency and effectiveness, between doing things faster and doing the right things, is the starting point for everything that follows.It's also, we'd argue, the starting point for this year’s PARC conference.

*We’ll be writing about the link between productivity and performance in our upcoming research paper to be published in early April.

PARC Conference — The Technology Paradox: Why More Investment Hasn't Delivered More Productivity

Wednesday 22 April 2026 | UCL Centre for Education, London